Every SPAC transaction eventually runs into the same question: will there be enough cash left in the trust to close the deal? Redemptions, market volatility, and shifting investor sentiment can all shrink the capital a SPAC has available at the moment it needs it most. This is where PIPE financing steps in. For sponsors, targets, and investors trying to understand how modern SPAC deals actually get done, PIPE financing isn’t a side note, it’s often the deal-maker. Here’s what it is, how it works, and why it has become a near-standard feature of SPAC transactions.

SPACs: A Refresher

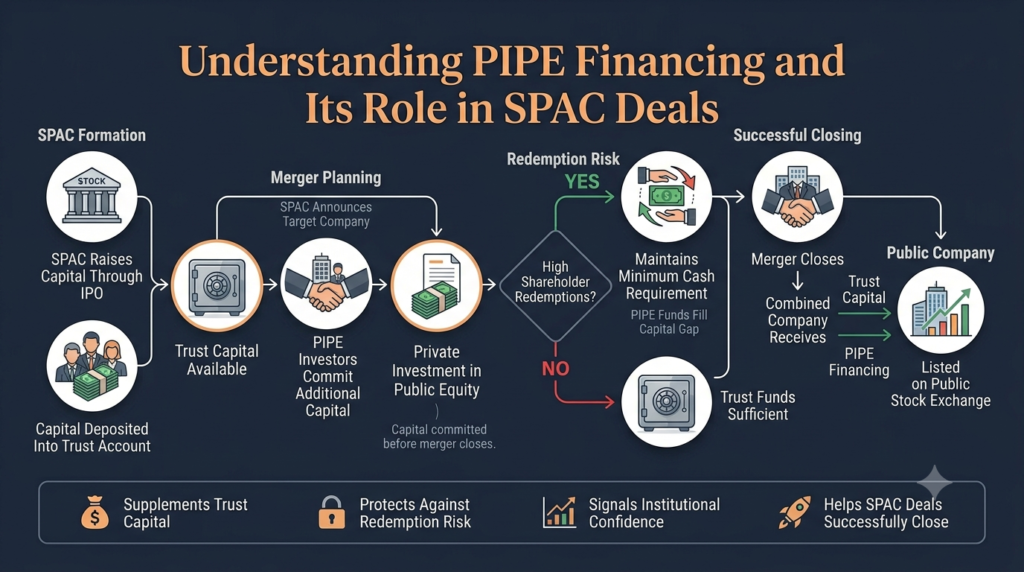

A Special Purpose Acquisition Company (SPAC) is a publicly listed shell company formed with one goal: to raise capital through an IPO and use that capital to acquire or merge with a private operating company, effectively taking it public. Investors in a SPAC’s IPO place their money in a trust account, and the SPAC’s sponsors have a set window, typically 18 to 24 months, to identify and complete a merger with a target company. If no deal is completed in that window, the trust is returned to shareholders.

SPAC vs. Traditional IPO: SPACs became popular because they offer private companies a faster, more negotiated path to public markets than a traditional IPO, along with more certainty around valuation. For sponsors, they represent an opportunity to build a platform, back a promising business, and share in its long-term upside.

What Is a PIPE Deal?

A PIPE, Private Investment in Public Equity, is a transaction in which institutional or accredited investors purchase shares (or convertible securities) directly from a publicly traded company, rather than through the open market. In the SPAC context, a PIPE investment is raised alongside the merger to supplement the capital sitting in the SPAC’s trust.

PIPE investors typically buy in at a fixed price, often the same price offered to original SPAC shareholders, and receive their shares through a private placement rather than a public offering. Because the transaction happens outside the public markets, it can be negotiated and closed quickly, without the extended timeline of a traditional secondary offering.

How PIPEs Work

The mechanics are straightforward. As a SPAC nears the announcement of a merger, its sponsors and the target company work with placement agents to line up PIPE investors, usually hedge funds, private equity firms, mutual funds, or other institutional players. These investors commit to purchasing a set dollar amount of shares at an agreed price, contingent on the SPAC merger closing.

The PIPE commitment is announced alongside the merger itself, giving the market an early signal of institutional confidence in the deal. Once the merger closes, the PIPE proceeds are added directly to the combined company’s balance sheet, alongside whatever capital remains in the SPAC’s trust after redemptions.

Why PIPEs Are Popular in SPAC Transactions

PIPE financing has become common in SPAC deals for a simple reason: redemptions are unpredictable. SPAC shareholders have the right to redeem their shares for a pro-rata portion of the trust instead of rolling into the merger, and in periods of market uncertainty, redemption rates can run high, sometimes emptying the majority of the trust. A PIPE gives sponsors and targets a way to backstop that risk with committed, contracted capital that doesn’t depend on how existing shareholders vote with their wallets.

Beyond filling potential funding gaps, PIPEs serve a signaling function. When sophisticated institutional investors commit capital to a deal before it closes, it tells the broader market, and remaining SPAC shareholders, that experienced allocators have done their own diligence and are willing to back the business. That validation can influence sentiment right when a deal needs it most.

How SPAC and PIPE Deals Work Together

The SPAC and PIPE structures are designed to complement each other. The SPAC provides the public listing vehicle and an initial pool of capital; the PIPE provides a flexible, negotiable layer of additional funding that can be sized to match the target’s actual capital needs. Sponsors typically begin PIPE discussions well before the merger is publicly announced, so that a committed PIPE amount can be disclosed at signing, giving the market clarity on total available capital from day one, rather than leaving it to be discovered at closing.

Redemption Risk as the Starting Point

Nearly every PIPE conversation in a SPAC deal starts with the same question: how much of the trust might be redeemed? Sponsors model a range of redemption scenarios and size the PIPE to ensure that even under a high-redemption outcome, the combined company will have enough cash to operate and meet its stated use-of-proceeds. Redemption risk isn’t a footnote in these negotiations, it’s the variable that shapes deal size, structure, and terms from the outset.

PIPE as a Market Validation Tool

Because PIPE investors conduct their own independent diligence before committing capital, a well-subscribed PIPE serves as a credibility marker for the target company. A strong PIPE roster, particularly one that includes recognizable institutional names, can reassure retail and existing shareholders that the deal has been vetted by parties with no incentive other than expected returns.

Closing Conditions and “Minimum Cash” Requirements

Most SPAC merger agreements include a minimum cash condition: a threshold of combined trust-plus-PIPE proceeds that must be met for the deal to close. If redemptions run high and the PIPE isn’t large enough to cover the shortfall, the deal can be at risk of falling through entirely, unless the parties renegotiate terms or bring in additional financing. This makes PIPE sizing one of the most closely watched elements of deal structuring, often finalized only in the final stretch before signing.

Practical Takeaways for Sponsors and Targets

For sponsors, the lesson is to start PIPE conversations early and build relationships with institutional investors well before a target is identified. For target companies, it’s worth understanding that a PIPE isn’t just a funding mechanism, it’s a diligence checkpoint that can shape valuation and deal terms. Both sides benefit from transparent, realistic redemption modeling rather than optimistic assumptions that leave the deal exposed at closing.

How Sandbridge Acquisition Approaches PIPE Structuring

At Sandbridge Acquisition, PIPE structuring is treated as a core part of deal architecture, not an afterthought bolted on near closing. Our team works to build investor relationships early, model redemption scenarios conservatively, and structure PIPE commitments that give target companies the confidence to move forward, even in choppier markets. That approach reflects a broader philosophy: a SPAC merger should be built to close on its stated terms, not hope its way across the finish line.

Conclusion

PIPE financing has moved from a supplemental tool to a foundational piece of how SPAC deals get done. By supplementing trust capital, absorbing redemption risk, and signaling institutional confidence, PIPEs give sponsors and targets the flexibility to structure deals that can withstand market volatility. Understanding how PIPEs work, and how they interact with SPAC mechanics, is essential for anyone evaluating or participating in a SPAC transaction today.