Special purpose acquisition companies raise money from public investors with a promise: your cash will either help fund a real business combination or come back to you. That promise is backed by a mechanism most retail investors never fully understand, the trust account. Paired with it is the redemption right, which lets shareholders pull their money out even if they don’t oppose a deal. Together, these two features are what separate a SPAC from a company going public the conventional way, and understanding them is essential before putting money into one.

Why the Trust Account Exists

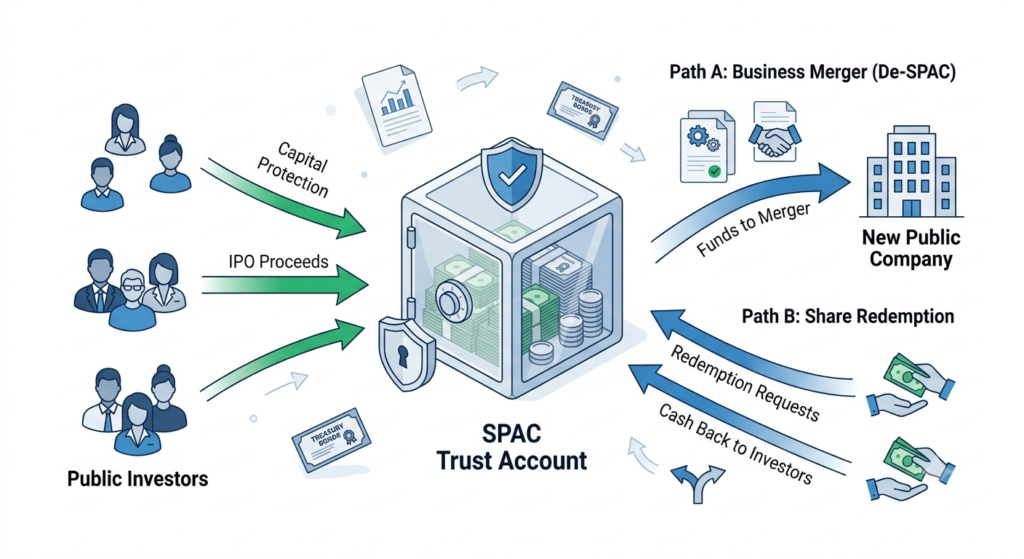

When a blank-check company completes its IPO, it isn’t handed a pile of cash to spend as it pleases. Nearly all of the money raised, often the full IPO amount and sometimes more, is placed into an interest-bearing trust account held by a third-party trustee. This structure exists specifically because a SPAC, by definition, has no operating business yet. If you want a refresher on what these vehicles are and why they’re structured this way in the first place, it helps to start with an overview of the blank-check company structure.

The trust typically holds the funds in short-term U.S. Treasury securities or government money market funds, chosen deliberately for their safety and liquidity rather than yield. The goal isn’t to generate outsized returns; it’s to preserve principal so that the amount available to shareholders doesn’t shrink meaningfully before a deal closes or the company liquidates. Interest earned in the trust generally accrues for the benefit of shareholders, though the SPAC sponsor is usually permitted to withdraw a limited amount to cover taxes and modest working capital needs.

Life of the Trust Before a Deal Closes

Once the money is in trust, it’s essentially locked. Sponsors cannot dip into it to pay salaries, marketing costs, or due diligence expenses on a potential target, those costs are covered separately, often from funds raised outside the trust or from sponsor loans. This separation is intentional: it ensures that even if the SPAC’s management team spends aggressively searching for a deal, shareholder capital stays protected.

SPACs typically have 18 to 24 months to find and complete a merger, though many charters allow extensions. When a SPAC asks shareholders to approve extra time, it often needs to deposit additional funds into the trust, sometimes a fixed amount per share, sometimes tied to how many shares remain outstanding. These extension payments matter because they directly affect the per-share value shareholders can later claim, and repeated extensions are one of the more common reasons trust economics change over the life of a SPAC.

What Actually Triggers a Redemption

Redemption rights are one of the more misunderstood features of SPAC investing. Many assume redeeming shares means voting against a deal, but the two are unrelated. A shareholder can vote in favor of a proposed merger and still choose to redeem their shares for cash. The redemption right is simply an option to exit at the shareholder’s discretion, exercisable around a few specific moments: the vote on a proposed business combination, a vote to extend the deadline, or the SPAC’s ultimate liquidation if no deal materializes in time.

This decoupling of voting and redeeming is deliberate. Securities rules require that shareholders be able to redeem regardless of how they vote, which prevents sponsors from effectively coercing approval by threatening to withhold liquidity from dissenters.

Walking Through the Redemption Process

The mechanics are more procedural than complicated. Ahead of a shareholder vote, the SPAC files proxy materials setting a specific deadline, usually a few business days before the meeting, by which shareholders must submit an election to redeem. This isn’t automatic; a shareholder has to instruct their broker to tender shares for redemption, and missing the deadline generally forfeits the right for that particular vote.

The redemption value itself is calculated by dividing the total trust balance by the number of shares eligible for redemption, net of any taxes owed and permitted withdrawals. In practice, this figure often lands close to, but not always exactly at, the original IPO price, since interest earned and extension deposits can push it slightly higher while taxes and fees can pull it down.

Once the deal closes and redemptions are processed, cash typically flows to redeeming shareholders within a matter of days. Their shares are canceled, reducing the total share count. Shareholders who chose not to redeem retain their equity in the newly public, merged company, holding a proportionally larger stake in what remains of the business.

Why Redemption Levels Can Make or Break a Deal

This is where trust account mechanics start to have real consequences for deal outcomes. If redemption rates run high, the trust can be drained well below what the target company needs to close the transaction. Most merger agreements include a minimum cash condition, and if too many shareholders cash out, that condition can be at risk.

To manage this, sponsors frequently line up outside the capital as a backstop. This is where private investment commitments negotiated alongside the merger come into play, supplying additional cash to replace what’s lost to redemptions and giving the combined company a more reliable capital base regardless of how shareholders vote. Deals with weak backstop arrangements are far more vulnerable to collapsing, or being renegotiated at less favorable terms, when redemptions spike.

Common Misunderstandings Worth Clearing Up

A few points trip up newer SPAC investors repeatedly. Redeeming isn’t a signal of opposition to a deal, it’s often just a way to capture close-to-guaranteed value while retaining warrants or rights that carry separate upside. The trust balance also isn’t a fixed, unchanging number; extension deposits, accrued interest, and permitted sponsor withdrawals all move it over time. And redemption is never automatic, shareholders who want their cash back must actively elect to redeem before the stated deadline, or they’ll simply carry their shares forward into the merged company by default.

The Bottom Line

Trust accounts and redemption rights exist to give SPAC investors a floor: a way to get much of their capital back if they don’t like the eventual deal, or if no deal happens at all. But the mechanics matter. How the trust is funded, how extensions erode or preserve it, and how heavily shareholders redeem all shape whether a business combination ultimately closes on the terms originally proposed. Investors who understand this plumbing are far better equipped to judge whether a SPAC investment is actually as low-risk as it’s often marketed to be.